Fund performance

Past performance is not indicative of future performance

# inception date was 29 March 2011

Performance Summary

Fund Liquidation

By now, all investors should have received a letter from Perpetual Trust Services Limited (the Responsible Entity), regarding the winding up of the Firstmac High Livez managed investment fund.

This follows our strategic decision to withdraw from investments and savings products.

We are proud of what we achieved with High Livez, always meeting our objectives of delivering a steady income to investors while protecting the value of their investments, and we were reluctant to wind up the fund.

However, due to its small size, the Fund’s ongoing operating costs make it commercially unviable for Firstmac to continue as investment manager.

We would like to thank all investors for their support of the Firstmac High Livez Fund over the past 13 years. We are saddened and disappointed that our fund has been brought to an end. We hope that Unit Holders will be able to find similar returns over equivalent low risk assets and recommend that you speak to your financial adviser.

During the month of October our Investment Committee has commenced the liquidation of fund assets. We have now reduced fund holdings of RMBS and ABS to 50.5% of total assets, with the balance held in cash. The remaining 50.5% of RMBS and ABS fund investments will be put to a market auction during the week of the 25th of November following expiration of the 30 days’ notice period to Unit Holders.

The sale of assets to date has gone well, with sale proceeds achieving above the September Unit Price values. We are pleased with this outcome.

This has resulted in a higher than usual monthly distribution for the month of October, with this months distributions including a combination of realised accrued interest and capital gains.

We provide the following breakdown of this month’s liquidation trading activities:

Fund Objective

The Trust aims to provide stable monthly income returns from a diversified portfolio of Asset-Backed Securities supplemented by a small allocation towards Short Term Money Market Securities.

The Trust will invest in Asset-Backed Securities and Short Term Money Market Securities which are normally only available to professional and institutional investors.

Our Investment Committee is pleased with the results of our fund, delivering on our objectives of capital stability and regular monthly income. We also maintain and manage liquidity closely across our fund should Unit Holders choose to redeem at any month end.

Fund Update

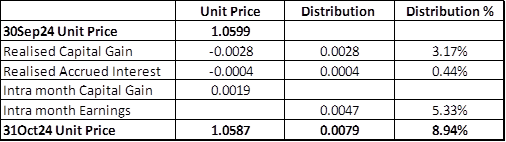

During October, the Fund Unit Price decreased from 1.0599 to 1.0587. This was actually a positive result as detailed in the table above. Essentially we have realised a part of the Unit Price premium above 100 (par) and have distributed this to Unit Holders, hence the higher monthly distribution of an annualised 8.94%. After accounting for the realised gains distributed to Unit Holders, the fund Unit Price actually improved by 0.18% (.0019 / 1.0599).

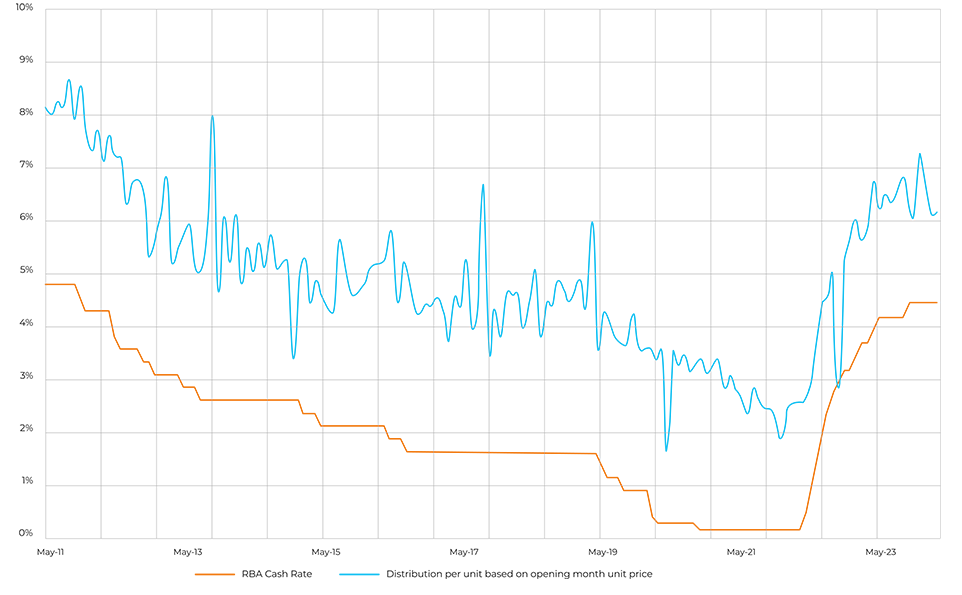

Unit Price volatility has remained low within a very narrow band. This is consistent with the fund objective of providing stable monthly income for our unit holders.

The fund has experienced low Unit Price volatility of an annualised 1% (calculated since August 2012). This means that the movement in Unit Price is quite narrow, tracking closely to the mean. This is consistent with a low risk managed fund.

For the month of October 2024, our fund distributed an annualised 8.94%. This record distribution includes realised gains and realised accrued interest as detailed in the above table.

The RBA Cash rate and BBSW1m are 99.4% correlated over a ten-year period. The RBA cash rate is widely understood and provides a useful explanation of fund returns, i.e. demonstrating that the fund returns are heavily influenced by changes in the RBA cash rate, as of course BBSW1m is highly correlated with the RBA cash rate.Underlying asset quality remains strong, with low delinquencies across the underlying residential mortgages. We are pleased with our portfolio resilience however we do anticipate some increase in delinquencies associated with increasing mortgage rates. We expect all investments to be comfortably within tolerance over the months ahead.

The Total Return for the past 10 years was 4.51% per annum.

It is recommended that unitholders invest with a timeframe of 3-5 years. Over the past year three years, the Total Return was 5.24% per year, and over the past five years was 4.44% per annum.

The High Livez Fund is not capital guaranteed.

Australian Economic Update

Australian economic indicators released in October continued to show the economy growing but at soft pace and inflation temporarily easing inside the RBA’s 2-3% target. September retail sales rose 0.1% m-o-m consolidating the 0.7% gain recorded in August. In volume terms, Q3 retail sales rose 0.5% q-o-q after falling 0.4% in Q2. Housing indicators were firm with the value of home loans up 0.1% m-o-m consolidating the 2.4% lift in August and a 4.4% m-o-m lift in home building approvals in September more than reversing a 3.9% fall in August. The labour market remained very tight, with employment up by 64,100 in September, the participation rate lifting to a record 67.2% and the unemployment rate unchanged at 4.1%. The Q3 CPI rose by 0.2% q-o-q reducing annual inflation to 2.8% y-o-y from 3.8% in Q2. The inflation reduction was due entirely to the effect of Government energy rebates. Underlying inflation measured by the trimmed mean rose 0.8% q-o-q in Q3 and by 3.5% y-o-y. monthly CPI showed a fall in headline annual inflation to 2.7% y-o-y in August The RBA’s November policy meeting this week is expected again to leave the cash rate unchanged at 4.35% and with renewed warning that any rate cut is still some way off.

Australian Credit Markets

Australian Tier 2 spreads rallied aggressively in October as the lack of Major Bank supply since July leaves the market in an excess demand position. Though we didn’t get Major Bank supply, there were three smaller regional/insurance A$ Tier 2 deals in October. The blistering pace of A$ securitisation issuance continued in October with another fourteen deals pricing. All up there was over A$11.3bn issued making it the busiest October ever and takes the YTD issuance over A$70bn for the first time (eclipsing an 18-year-old record of A$64.1bn set in 2006). Unlike September that saw six auto and credit card ABS deals, October was heavily dominated by RMBS which made up twelve of the fourteen deals. With a lot of issuers intentionally getting their deals done ahead of this week’s US election, the pace of issuance is likely to slow in November.

Historical performance assumptions

*Total Return for the 10 years to 31 October 2024 and 5.45% since inception on 29 March 2011. The total return is the Fund’s consolidated performance over the period referenced. Performance is calculated on an initial investment of $10,000 with distributions reinvested. Ongoing fees and expenses have been applied however individual taxes are excluded. This website is prepared and issued by Firstmac Limited ACN 094 145 963 (Firstmac) the holder of Australian financial services licence (AFSL) number 290600 in respect of Firstmac High Livez ARSN 147 322 923 (Fund). Perpetual Trust Services Limited ACN 000 142 049, the holder of AFSL number 236648 is the responsible entity (RE) and the issuer of the units in the Fund (Units). A target market determination for the Fund is available at www.firstmac.com.au or by contacting Firstmac on 13 12 20. This website has been prepared without taking account of your objectives, financial situation or needs. Before investing in the Fund, you should consider whether an investment in the Fund is appropriate having regards to your objectives, financial situation and needs and obtain appropriate professional advice. Prior to making a decision about whether to acquire, hold or dispose of Units you should consider the product disclosure statement (PDS) for the Fund available at www.firstmac.com.au. Past performance is not a reliable indicator of future performance and may not be repeated. Restrictions may apply to the amount and timing of withdrawal requests – refer to the PDS for full details.

Welcome to firstmac.com.au _

Just in case we lose you, may I ask for your contact details....